What Is Double Entry Bookkeeping?

In Principles of Accounts (POA), every financial transaction affects two accounts. This system is called double entry bookkeeping. For every entry made on one side, an equal and opposite entry is made on the other side.

This is the foundation of all accounting. Once you understand double entry, the rest of POA becomes much easier to follow.

Definition — Double Entry

Double entry means every transaction is recorded twice — once as a debit in one account and once as a credit in another account. The total debits must always equal the total credits.

The Accounting Equation

All of POA is built on one equation:

This equation must always balance. When you record a transaction correctly using double entry, the equation stays balanced.

- Assets — things the business owns (cash, equipment, inventory, debtors)

- Liabilities — things the business owes (creditors, loans, bank overdraft)

- Owner's Equity / Capital — what the owner has invested plus retained profit

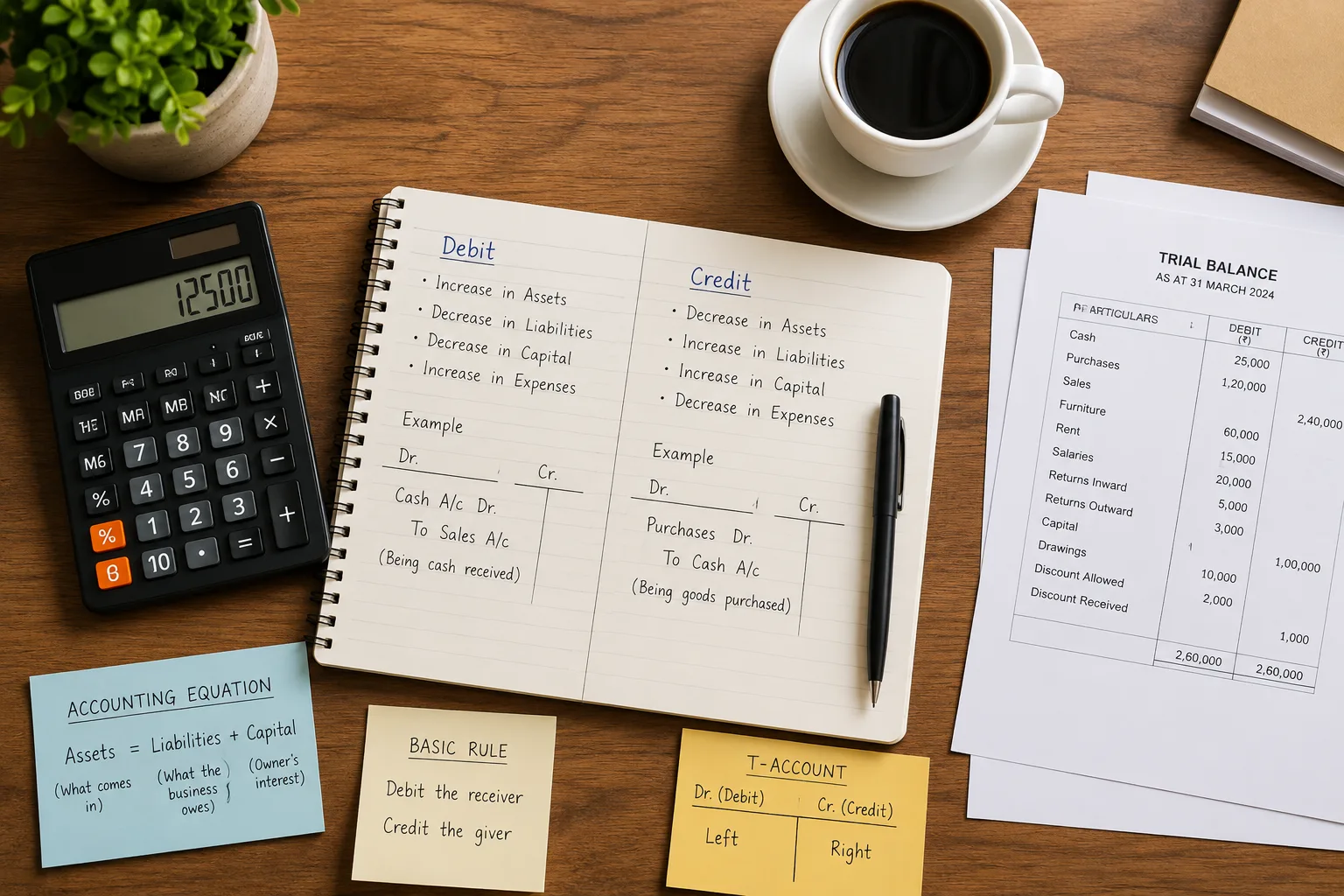

Debit and Credit Rules POA Students Must Know

Every account in accounting has two sides — a left side (debit side) and a right side (credit side). The words "debit" and "credit" simply mean left and right in accounting. They do not mean "good" or "bad".

Debit (Dr)

An entry on the left side of an account. Debits increase assets and expenses. Debits decrease liabilities, capital, and income.

Credit (Cr)

An entry on the right side of an account. Credits increase liabilities, capital, and income. Credits decrease assets and expenses.

The rules summarised:

- Assets: Debit to increase, Credit to decrease

- Liabilities: Credit to increase, Debit to decrease

- Capital / Equity: Credit to increase, Debit to decrease

- Income / Revenue: Credit to increase, Debit to decrease

- Expenses: Debit to increase, Credit to decrease

Worked Examples

Example 1 — Cash purchase of equipment

A business pays $500 cash to buy a printer.

- Equipment (Asset) increases → Debit Equipment $500

- Cash (Asset) decreases → Credit Cash $500

Example 2 — Owner invests capital

Owner puts $10,000 into the business bank account.

- Bank (Asset) increases → Debit Bank $10,000

- Capital (Equity) increases → Credit Capital $10,000

Example 3 — Credit purchase from supplier

Business buys $800 of inventory on credit from a supplier.

- Purchases (Expense) increases → Debit Purchases $800

- Creditor (Liability) increases → Credit Creditor $800

Example 4 — Cash sales

Business sells goods for $1,200 cash.

- Cash (Asset) increases → Debit Cash $1,200

- Sales (Income) increases → Credit Sales $1,200

Ledger Accounts and the T-Account

A ledger account is often drawn as a T-shape. The left side is always Debit and the right side is always Credit.

To find the balance of an account:

- Add up all entries on the debit side.

- Add up all entries on the credit side.

- The larger total is the balance side. Write "Balance c/d" on the smaller side to make both totals equal.

- Bring the balance down (Balance b/d) on the opposite side, ready for the next period.

Common Mistakes in POA

- Reversing debit and credit — the most common error. Always check: does this account increase or decrease? Then apply the correct rule.

- Treating drawings as expenses — drawings reduce capital, not profit. They go in the capital account or drawings account, not the income statement.

- Forgetting to balance the ledger — every account must be balanced and brought down at the end of the period.

- Confusing debtors and creditors — debtors owe the business money (asset). Creditors are owed money by the business (liability).

- Putting returns in the wrong account — returns inward (sales returns) reduce sales. Returns outward (purchase returns) reduce purchases.

Practice Questions

- A business pays $300 rent in cash. Which account is debited and which is credited? Explain your answer.

- A customer owes the business $600 and pays by cheque. Record the journal entry.

- The business buys equipment worth $2,000 on credit. Record the double entry.

- The owner withdraws $400 cash for personal use. What is the effect on assets and capital?

- Sales for the month total $5,500. Returns inward amount to $200. What is the net sales figure?

What Comes Next in POA

Once you are confident with debit and credit, you will move on to:

- Trial balance — checking that total debits equal total credits

- Income statement — calculating gross profit and net profit

- Balance sheet — showing the financial position of the business

- Bank reconciliation — matching the cash book with the bank statement

Strong-Willed Tutoring Services provides structured Principles of Accounts tuition that covers all O-Level POA topics with clear explanations and exam-focused practice. For students who need to build their debit and credit foundation, our O-Level POA tuition programme is the right place to start.

N-Level POA: Understanding Inventories and Trade Receivables

Two important topics in the N-Level Principles of Accounts (POA) syllabus are Inventories and Trade Receivables. These topics are essential because they affect a business's profit, financial position, and cash flow. Understanding how inventories and trade receivables are recorded and managed helps students answer examination questions accurately and understand how businesses operate in the real world.

What Are Inventories?

Inventories are goods that a business purchases or produces for the purpose of selling to customers.

For example: a bookstore's inventories are books; a clothing shop's inventories are clothes; a grocery store's inventories are food and household products.

Inventories are classified as a current asset because they are expected to be sold within one accounting period.

Cost of Goods Sold (COGS)

When inventories are sold, the cost of those inventories becomes an expense known as Cost of Goods Sold (COGS).

Formula — Cost of Goods Sold

Cost of Goods Sold = Opening Inventory + Purchases − Closing Inventory

Example:

- Opening Inventory: $5,000

- Purchases: $15,000

- Closing Inventory: $4,000

- Cost of Goods Sold = $5,000 + $15,000 − $4,000 = $16,000

Closing Inventory

Closing Inventory refers to inventories remaining unsold at the end of the accounting period. It appears in the Statement of Financial Position as a Current Asset and is deducted when calculating Cost of Goods Sold.

A higher closing inventory generally results in a lower cost of goods sold and a higher gross profit.

What Are Trade Receivables?

Trade Receivables are customers who owe money to the business because they purchased goods on credit. Trade receivables were previously known as debtors.

Example

ABC Trading sells goods worth $2,000 to a customer on credit. The customer does not pay immediately. ABC Trading records Trade Receivables = $2,000.

Businesses may offer credit to attract customers, increase sales, and build long-term business relationships. However, selling on credit also creates risk because customers may delay payment or fail to pay altogether.

Trade receivables are classified as a current asset because the business expects to collect the money within one year.

Allowance for Impairment of Trade Receivables

Not all customers pay their debts. Businesses therefore estimate potential losses using an Allowance for Impairment of Trade Receivables. This follows the accounting principle of prudence — anticipating possible losses.

Example

Trade Receivables = $10,000 | Allowance for Impairment = $500 | Net Trade Receivables = $10,000 − $500 = $9,500

Bad Debts

A Bad Debt occurs when a customer is unable to pay and the amount becomes irrecoverable.

- A customer owes $300 and goes bankrupt — the business writes off the debt.

- Journal Entry: Dr Bad Debts Expense $300 | Cr Trade Receivables $300

Examination Example

A business reports: Opening Inventory $8,000 | Purchases $25,000 | Closing Inventory $6,000 | Trade Receivables $12,000 | Allowance for Impairment $400.

- Cost of Goods Sold = $8,000 + $25,000 − $6,000 = $27,000

- Net Trade Receivables = $12,000 − $400 = $11,600

At Strong-Willed Tutoring Services, students learn these concepts through clear explanations, worked examples, and intensive practice using examination-style questions aligned with the latest Singapore MOE syllabus.