Introduction

A Bank Reconciliation Statement (BRS) is one of the most important topics in O-Level Principles of Accounts. Businesses often discover differences between their Cash at Bank account and the bank statement balance. These differences occur because certain transactions may not yet have been recorded by either the business or the bank.

Understanding how to prepare a Bank Reconciliation Statement is essential for examination success and for maintaining accurate financial records.

Definition — Bank Reconciliation Statement

A Bank Reconciliation Statement is a document that explains and reconciles the difference between the balance shown in the business's Cash at Bank account and the balance shown on the bank statement at the same date.

Why Do Differences Occur?

Common reasons include:

- Unpresented cheques — cheques issued by the business but not yet presented to the bank for payment

- Deposits not yet credited — deposits made by the business but not yet shown on the bank statement

- Bank charges — fees deducted by the bank but not yet recorded in the Cash at Bank account

- Interest received — interest credited by the bank but not yet recorded in the books

- Direct debits and standing orders — automatic payments recorded by the bank but not yet entered in the books

- Errors — mistakes made by the business or the bank

Purpose of a Bank Reconciliation Statement

The Bank Reconciliation Statement helps to:

- Verify the accuracy of accounting records

- Detect errors in either the Cash at Bank account or the bank statement

- Identify transactions omitted from either set of records

- Ensure the correct cash balance is reported in financial statements

Two Types of Differences

Timing Differences

These occur because the business and the bank record the same transaction at different times. Examples: unpresented cheques and deposits not yet credited. These do NOT require any correction to the Cash at Bank account.

Errors and Omissions

These occur when a transaction has been omitted or recorded incorrectly. These REQUIRE a correcting journal entry to update the Cash at Bank account before preparing the reconciliation statement.

Steps to Prepare a Bank Reconciliation Statement

- Update the Cash at Bank account for any items appearing on the bank statement but not yet recorded in the books (bank charges, interest, direct debits, errors).

- Calculate the revised Cash at Bank balance after updating.

- Start with the revised Cash at Bank balance (or the bank statement balance — depending on the format required).

- Add: deposits not yet credited (outstanding lodgements).

- Less: unpresented cheques.

- The result should equal the other balance — if it does, the reconciliation is complete.

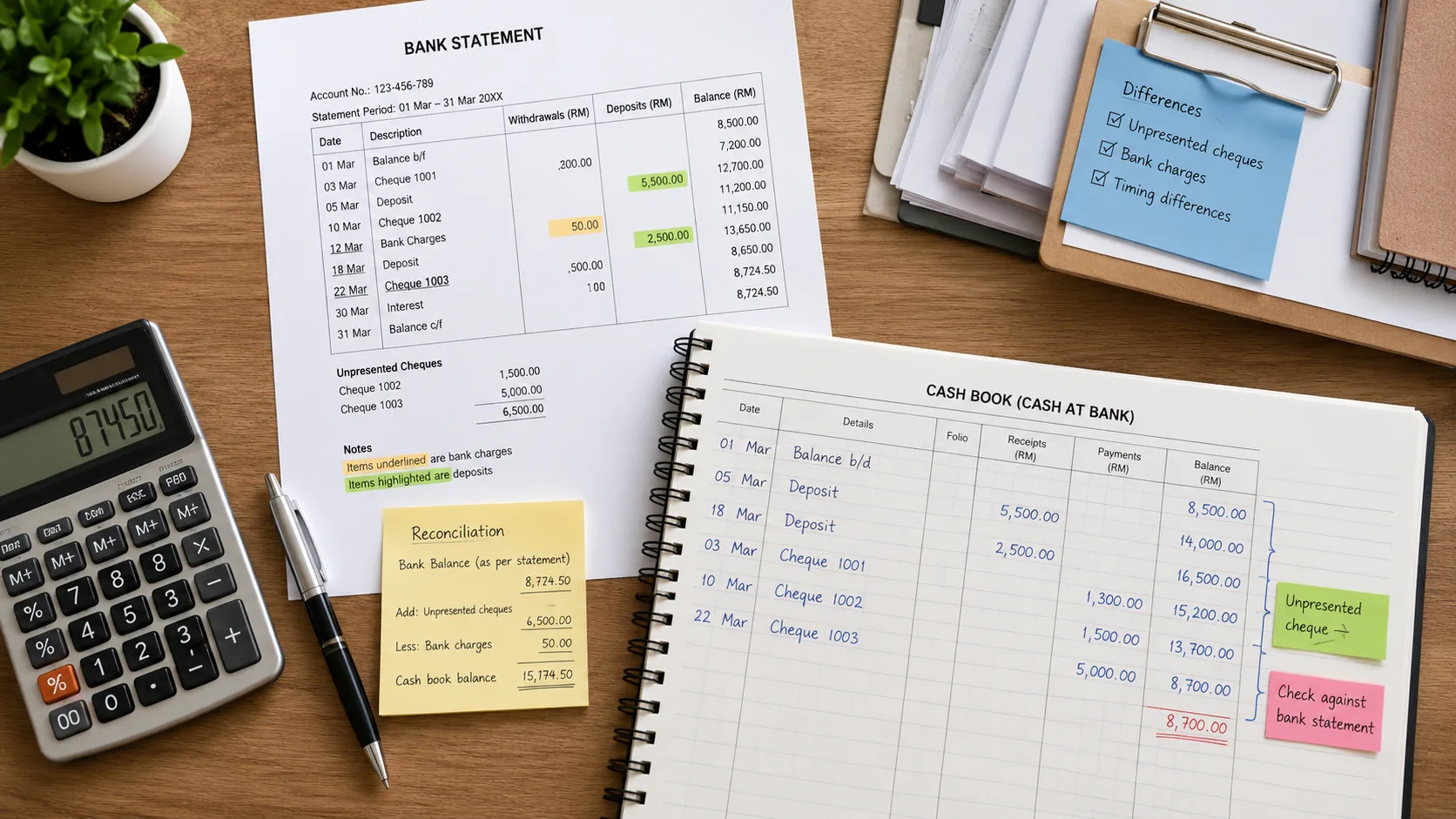

Worked Example

At 31 December, the Cash at Bank account shows a balance of $3,200 (debit). The bank statement shows a balance of $3,800.

Investigation reveals:

- Bank charges of $50 appear on the bank statement but have not been recorded in the books.

- A direct debit of $100 appears on the bank statement but has not been recorded.

- Unpresented cheques total $700.

- A deposit of $350 made on 31 December does not appear on the bank statement.

Step 1 — Update Cash at Bank account:

- Cash at Bank per books: $3,200

- Less bank charges: −$50

- Less direct debit: −$100

- Revised Cash at Bank balance: $3,050

Step 2 — Prepare Bank Reconciliation Statement:

- Balance per bank statement: $3,800

- Add deposits not yet credited: +$350

- Less unpresented cheques: −$700

- Reconciled balance (should equal revised Cash at Bank): $3,450

Common Bank Reconciliation Mistakes in O-Level POA

- Updating the bank statement balance for items that only affect the books — bank charges and direct debits update the books, not the bank statement side.

- Confusing unpresented cheques with outstanding deposits — unpresented cheques are deducted from the bank statement balance; outstanding deposits are added.

- Forgetting to update the Cash at Bank account first — many students skip this step and cannot reconcile correctly.

- Treating the reconciliation statement as a ledger account — it is a statement, not a ledger account; debit and credit labels do not apply.

Practice Questions

- The Cash at Bank account shows $4,500 (debit). The bank statement shows $5,100. Unpresented cheques total $800. Bank charges are $200. What is the revised Cash at Bank balance?

- List three items that would require an update to the Cash at Bank account before preparing the reconciliation.

- What is the difference between a timing difference and an error in a bank reconciliation?

- A deposit of $600 was recorded on 30 December but does not appear on the bank statement dated 31 December. How is this treated in the reconciliation?

Need Help with O-Level POA Tuition?

If your child needs help with bank reconciliation, Strong-Willed Tutoring Services provides O-Level POA tuition in Singapore with step-by-step guidance and exam-style practice. View our tuition fees or enquire now.

Conclusion

Bank reconciliation is a highly tested topic at O-Level and requires careful attention to detail. Regular practice will help students become confident in handling examination questions. At Strong-Willed Tutoring Services, we work through real examination-style questions so students can apply this method accurately under exam conditions.