Introduction

Businesses use non-current assets such as machinery, vehicles, and office equipment over many years. As these assets are used, they lose value over time. This decrease in value is known as depreciation.

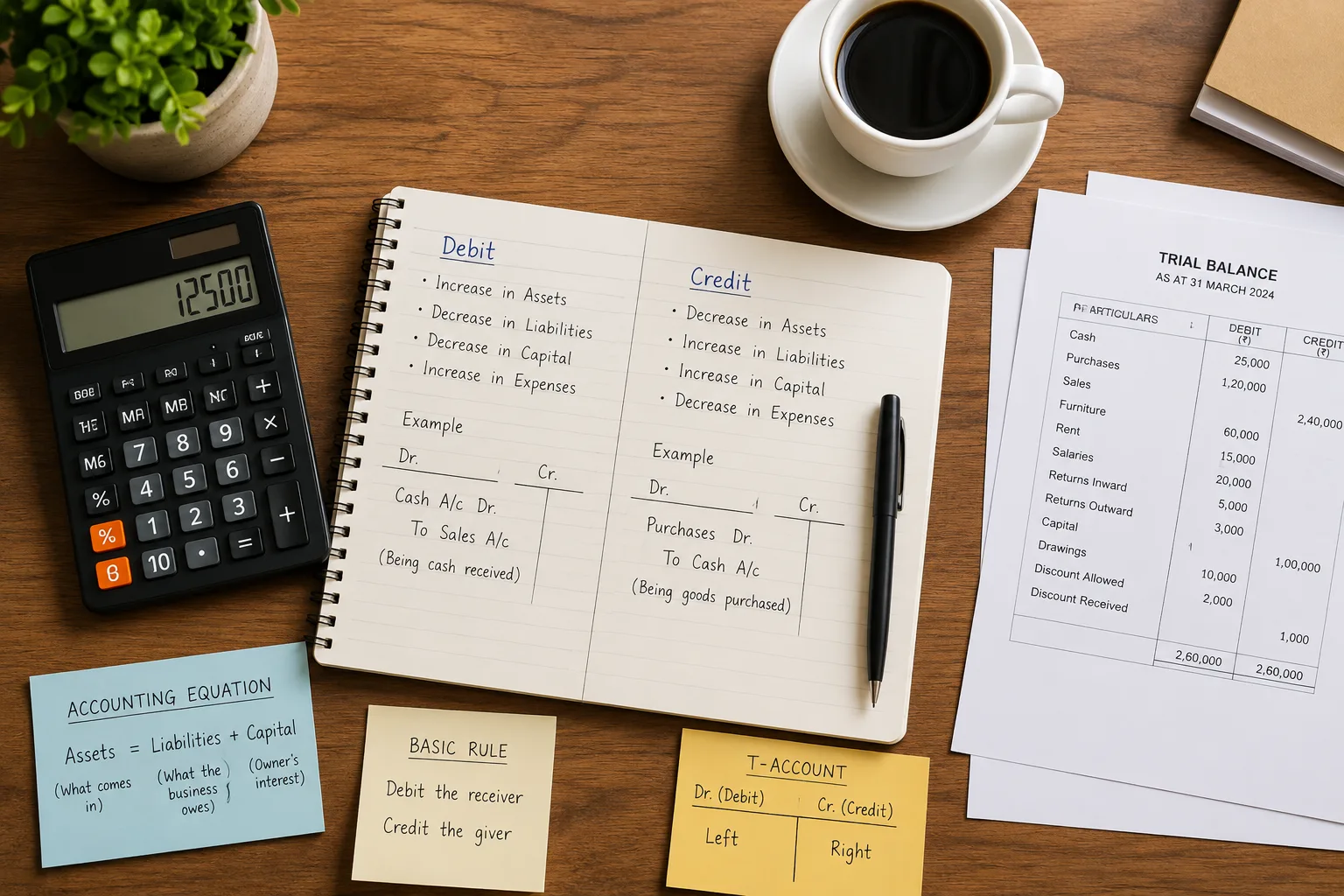

Definition — Depreciation

Depreciation is the systematic allocation of the cost of a non-current asset over its useful life. It represents the portion of the asset's value used up during each accounting period.

Why Is Depreciation Necessary?

Depreciation ensures that:

- The cost of an asset is spread over its useful life (matching principle)

- Profit is not overstated by treating the full cost as an expense in one year

- Financial statements provide a fair view of the business's assets and performance

- The carrying amount of assets in the balance sheet reflects a realistic value

Common Causes of Depreciation

- Wear and tear — physical deterioration from use

- Obsolescence — assets become outdated due to new technology

- Passage of time — some assets lose value simply over time (e.g., leases)

- Depletion — natural resources (e.g., mines) used up over time

Key Terms

- Cost — the original purchase price of the asset including installation and delivery

- Residual Value (Scrap Value) — the estimated amount the asset will be worth at the end of its useful life

- Useful Life — the number of years the business expects to use the asset

- Carrying Amount (Net Book Value) — Cost minus Accumulated Depreciation

- Accumulated Depreciation — total depreciation charged on an asset since it was purchased

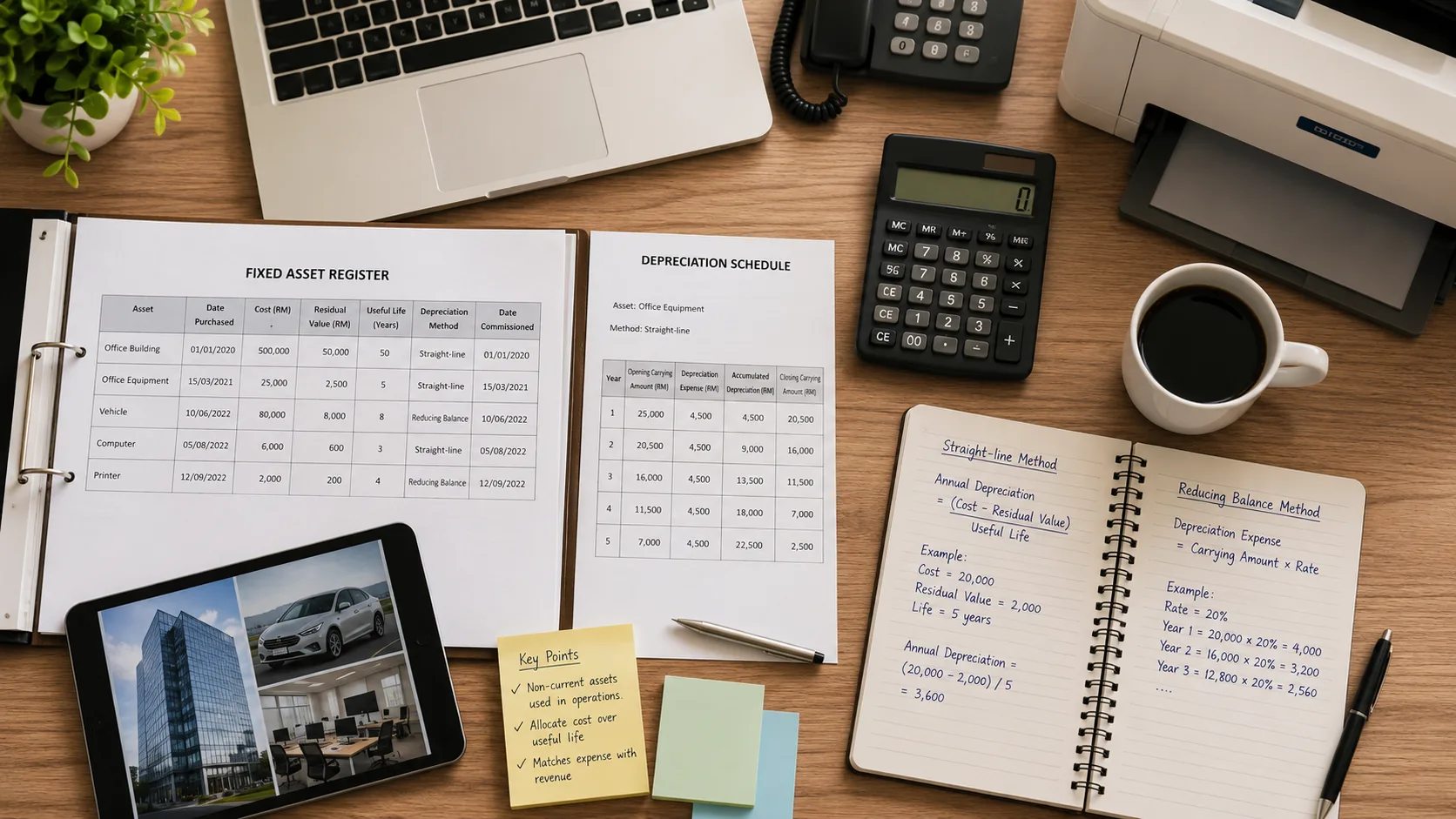

Depreciation of Non-Current Assets POA Examples

Under this method, the same amount of depreciation is charged every year throughout the asset's useful life.

Formula — Straight-Line Method

Annual Depreciation = (Cost − Residual Value) ÷ Useful Life

Example:

- Cost = $10,000

- Residual Value = $1,000

- Useful Life = 3 years

- Annual Depreciation = ($10,000 − $1,000) ÷ 3 = $3,000 per year

Depreciation Schedule (Straight-Line):

- Year 1: Depreciation $3,000 | Carrying Amount $7,000

- Year 2: Depreciation $3,000 | Carrying Amount $4,000

- Year 3: Depreciation $3,000 | Carrying Amount $1,000 (residual value)

Reducing Balance Method

Under this method, depreciation is calculated each year as a fixed percentage of the carrying amount (not the original cost). The depreciation charge decreases each year as the carrying amount falls.

Formula — Reducing Balance Method

Annual Depreciation = Carrying Amount at Start of Year × Depreciation Rate (%)

Example:

- Cost = $10,000

- Depreciation Rate = 40% per year

- Year 1: $10,000 × 40% = $4,000 | Carrying Amount = $6,000

- Year 2: $6,000 × 40% = $2,400 | Carrying Amount = $3,600

- Year 3: $3,600 × 40% = $1,440 | Carrying Amount = $2,160

Journal Entries for Depreciation

At the end of each accounting period, record depreciation with the following journal entry:

- Dr Depreciation Expense (amount)

- Cr Accumulated Depreciation (amount)

The Depreciation Expense appears in the Income Statement as an expense, reducing profit. Accumulated Depreciation appears in the Balance Sheet as a deduction from the cost of the asset to show the carrying amount.

Disposal of Non-Current Assets

When a non-current asset is sold or scrapped, the business removes it from the books using a Disposal Account.

- Transfer the asset cost to the Disposal Account: Dr Disposal | Cr Asset at Cost

- Transfer accumulated depreciation: Dr Accumulated Depreciation | Cr Disposal

- Record the proceeds received: Dr Cash/Bank | Cr Disposal

- Close the Disposal Account — the balance is a profit or loss on disposal

Common Mistakes

- Using the wrong base for reducing balance — always apply the rate to the carrying amount, not the original cost.

- Forgetting to deduct the residual value — the residual value is only deducted in the straight-line formula; it is not used in the reducing balance formula.

- Confusing depreciation expense with accumulated depreciation — depreciation expense is the charge for the current year; accumulated depreciation is the total charged since purchase.

- Depreciating land — land is not depreciated; only buildings and other non-current assets are.

Practice Questions

- A machine costs $15,000. Residual value is $3,000. Useful life is 4 years. Calculate the annual depreciation using the straight-line method.

- A vehicle costs $20,000. Depreciation rate is 25% per year (reducing balance). Calculate the depreciation for Year 1 and Year 2.

- What journal entries are needed to record depreciation of $2,500 at the end of the financial year?

- An asset with a carrying amount of $5,000 is sold for $4,200. Calculate the profit or loss on disposal.

- Why might a business choose the reducing balance method over the straight-line method for motor vehicles?

Students who need additional guidance on depreciation of non-current assets, journal entries, and disposal questions can get structured support through O-Level POA tuition at Strong-Willed Tutoring Services.

Conclusion

Depreciation is a fundamental accounting concept and regularly appears in O-Level examinations. Students should master both calculation methods and journal entries. At Strong-Willed Tutoring Services, we practise all depreciation question types — schedule preparation, journal entries, ledger accounts, and disposal — so students are fully prepared for the examination.