Introduction

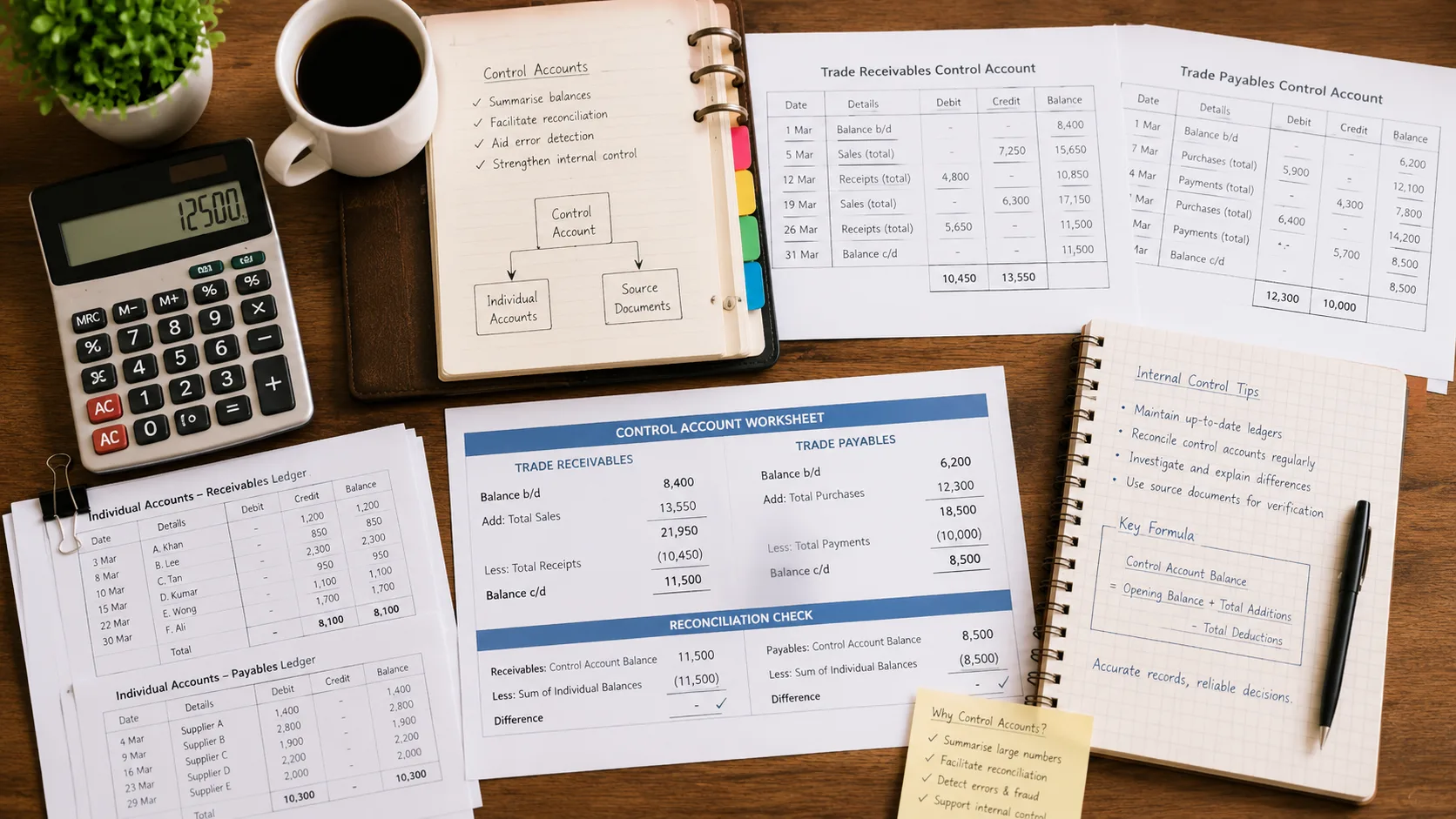

Control Accounts help businesses manage large numbers of trade receivables and trade payables efficiently. Instead of posting every individual transaction directly to the main ledger, businesses maintain individual accounts in a subsidiary ledger and summarise the totals in a Control Account in the main ledger.

Definition — Control Account

A Control Account is a summary account in the main (general) ledger that records the total of all transactions affecting a group of similar accounts held in a subsidiary ledger. The balance on the Control Account should equal the total of all individual balances in the subsidiary ledger.

The Two Common Control Accounts

In O-Level POA, you need to know two main control accounts:

- Trade Receivables Control Account (also called Sales Ledger Control Account) — summarises all amounts owed to the business by customers

- Trade Payables Control Account (also called Purchases Ledger Control Account) — summarises all amounts owed by the business to suppliers

Advantages of Control Accounts

- Improved accuracy — errors can be detected quickly by comparing the control account balance with the total of the subsidiary ledger

- Division of work — different staff can maintain the subsidiary ledger and the main ledger, strengthening internal control

- Faster preparation of financial statements — the control account balance can be used directly without adding up all individual accounts

- Fraud prevention — separating duties reduces the risk of fraud because no single person controls both sets of records

Trade Receivables Control Account — Common Entries

Debit Side (increases trade receivables)

Opening balance | Credit sales | Dishonoured cheques | Interest charged to customers

Credit Side (decreases trade receivables)

Cash and cheques received from customers | Discounts allowed | Returns inwards (sales returns) | Bad debts written off | Closing balance

Worked Example — Trade Receivables Control Account:

- Opening balance: $12,000

- Credit sales during month: $45,000

- Cash received from customers: $38,000

- Discounts allowed: $500

- Returns inwards: $800

- Bad debts written off: $200

Closing balance = $12,000 + $45,000 − $38,000 − $500 − $800 − $200 = $17,500

Trade Payables Control Account — Common Entries

Credit Side (increases trade payables)

Opening balance | Credit purchases | Returns inwards from business to supplier being reversed

Debit Side (decreases trade payables)

Cash and cheques paid to suppliers | Discounts received | Returns outwards (purchase returns) | Closing balance

Worked Example — Trade Payables Control Account:

- Opening balance: $8,000

- Credit purchases during month: $22,000

- Cash paid to suppliers: $18,000

- Discounts received: $400

- Returns outwards: $600

Closing balance = $8,000 + $22,000 − $18,000 − $400 − $600 = $11,000

Reconciling Control Account with Subsidiary Ledger

If the control account balance does not equal the total of the subsidiary ledger balances, there is an error somewhere. Common causes include:

- A transaction posted to the control account but not to the individual account in the subsidiary ledger (or vice versa)

- An incorrect amount posted to either the control account or the subsidiary ledger

- A posting to the wrong side of an account

Special Items — Dishonoured Cheques

A dishonoured cheque (bounced cheque) means the customer's payment was not honoured by the bank. The business must:

- Reverse the original cash receipt: Dr Trade Receivables | Cr Cash/Bank

- This increases the trade receivables balance — the customer still owes the money.

- In the control account, a dishonoured cheque appears on the debit side (increases receivables).

POA Control Accounts Common Mistakes Students Should Avoid

- Placing discounts on the wrong side — discounts allowed reduce receivables (credit side); discounts received reduce payables (debit side).

- Confusing returns inwards and returns outwards — returns inwards (from customers) reduce receivables; returns outwards (to suppliers) reduce payables.

- Forgetting dishonoured cheques — dishonoured cheques increase receivables (debit side) because the original receipt must be reversed.

- Treating contra entries incorrectly — a contra entry occurs when the same business is both a customer and a supplier; it reduces both the receivables and payables control accounts.

Practice Questions

- On which side of the Trade Receivables Control Account would you record: (a) credit sales, (b) cash received from customers, (c) discounts allowed, (d) bad debts written off?

- The Trade Receivables Control Account has an opening balance of $9,500. Credit sales are $32,000. Cash received is $28,500. Discounts allowed are $600. Returns inwards are $400. Calculate the closing balance.

- What is a contra entry and how is it recorded in the control accounts?

- A customer's cheque for $1,200 is dishonoured. How should this be recorded in the Trade Receivables Control Account?

- State two advantages of maintaining control accounts.

Students who struggle with trade receivables and trade payables control accounts can benefit from structured POA tuition in Singapore. Explore our O-Level POA tuition programme or view our tuition fees.

Conclusion

Control Accounts are a common O-Level examination topic and help students understand how businesses maintain accurate accounting records while managing large numbers of customer and supplier accounts. At Strong-Willed Tutoring Services, we practise all control account formats and reconciliation questions to ensure students are confident for their O-Level examinations.