Introduction

Even experienced accountants make mistakes. The Correction of Errors topic teaches students how to identify and rectify accounting errors while maintaining accurate financial records. This is a problem-solving topic that requires logical thinking and strong double-entry bookkeeping skills.

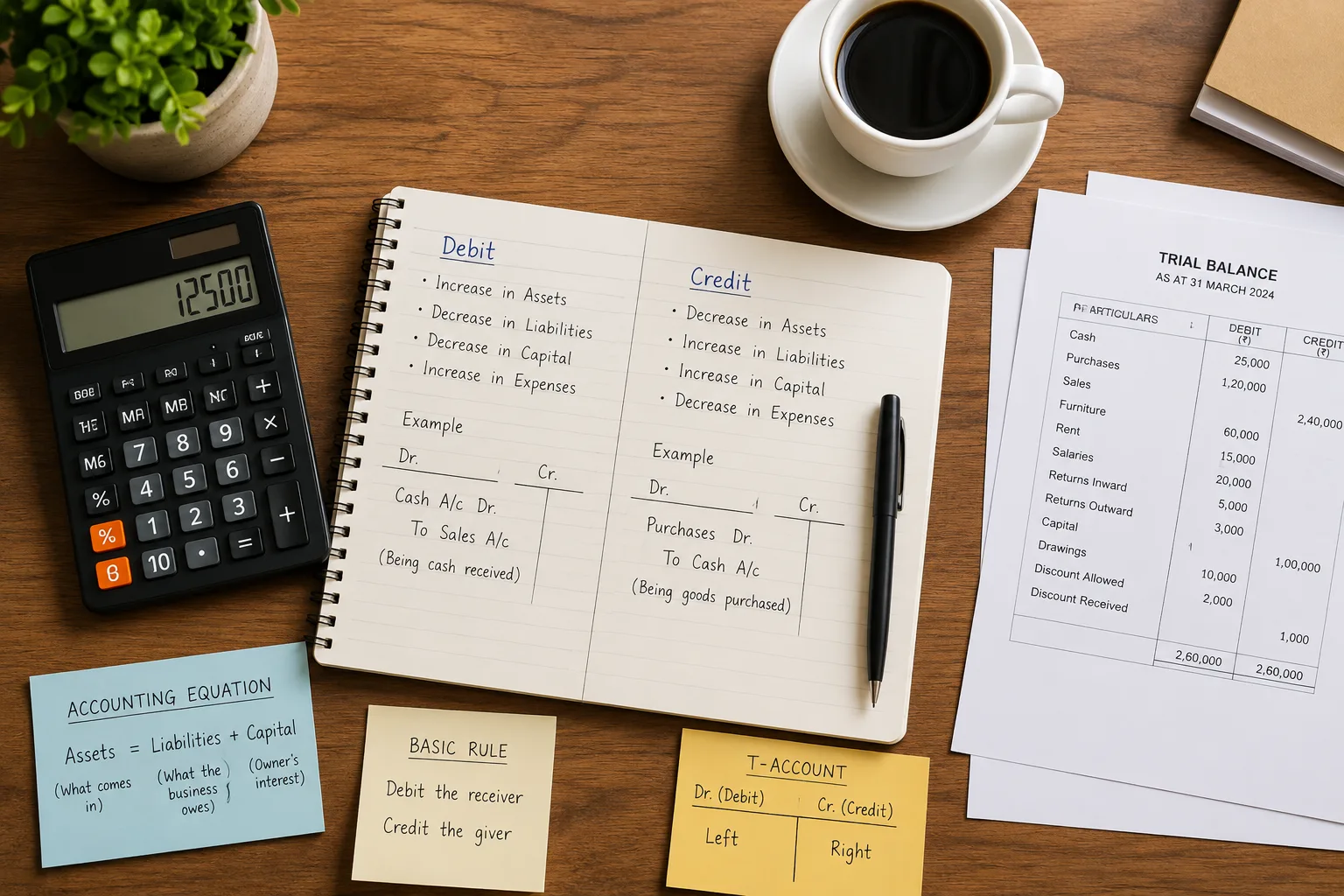

The Trial Balance and Errors

A trial balance is a list of all account balances. If total debits equal total credits, the trial balance is said to agree. However, a trial balance that agrees does not guarantee that all entries are correct — some errors are not detected by the trial balance.

Errors that DO NOT affect the trial balance agreement

Error of omission, error of commission, error of principle, error of original entry (both sides wrong by same amount), complete reversal of entries, compensating errors.

Errors that DO affect the trial balance agreement

Single-sided entries, posting to the wrong side of the correct account, arithmetic errors in one account only, errors of partial omission (one entry made, other missing).

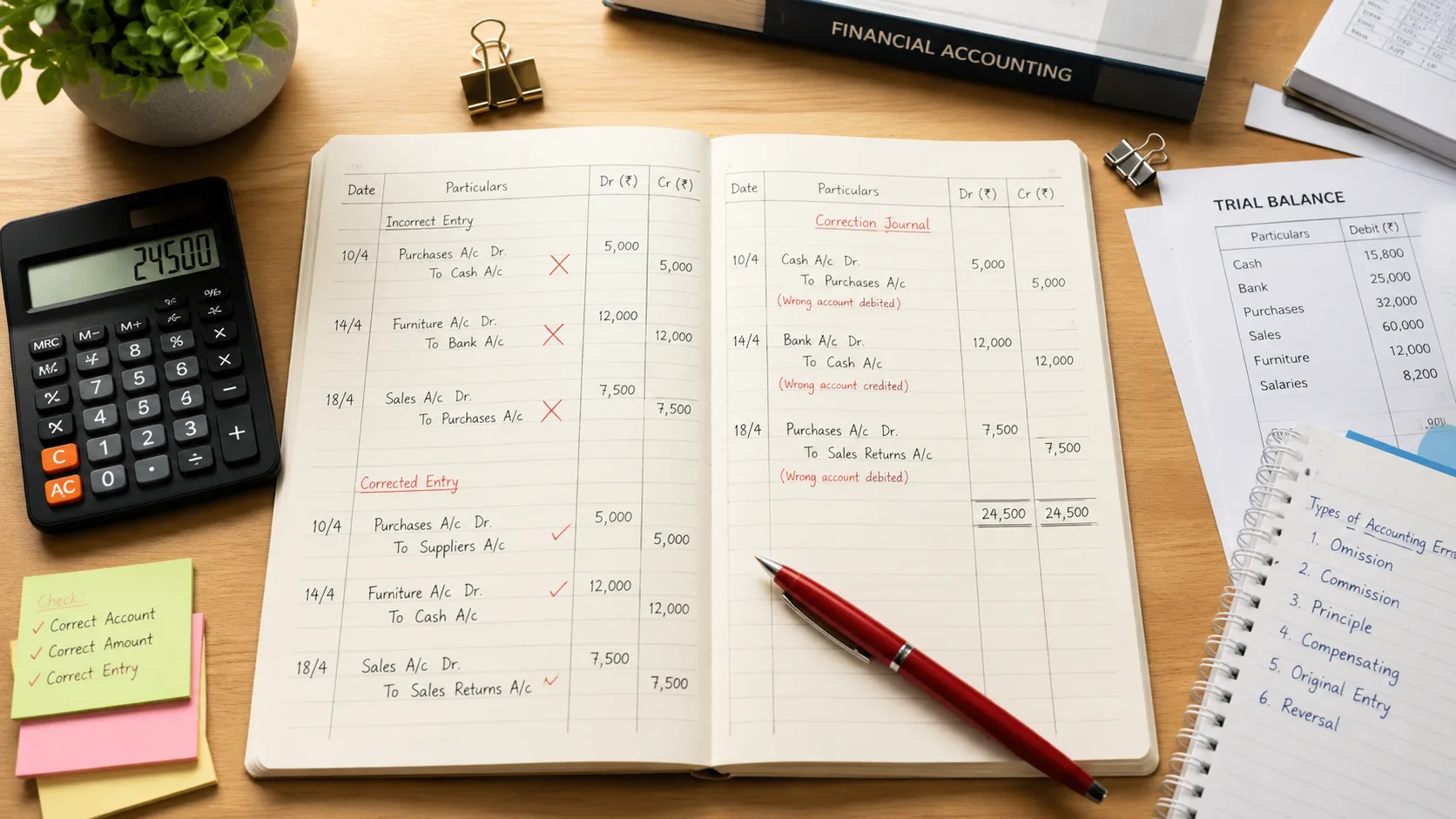

Correction of Errors Ledger Entry Guide

1. Error of Omission

A transaction is completely omitted from the accounting records. Both the debit and credit entries are missing.

Example: A credit sale of $500 to customer Lee was not recorded at all.

Correction: Dr Trade Receivables (Lee) $500 | Cr Sales $500

2. Error of Commission

A transaction is recorded in the wrong account of the correct type. Both debit and credit entries are made but in the wrong personal account.

Example: A payment from customer Tan of $300 was credited to customer Lim's account instead.

Correction: Dr Lim $300 | Cr Tan $300

3. Error of Principle

A transaction is recorded in the wrong type of account, violating accounting principles. For example, a capital expenditure is treated as a revenue expense.

Example: The purchase of office furniture ($2,000) was debited to Office Expenses instead of Furniture.

Correction: Dr Furniture $2,000 | Cr Office Expenses $2,000

4. Error of Original Entry

The wrong amount is entered in both accounts. The trial balance still agrees because both debit and credit are wrong by the same amount.

Example: Cash sales of $750 were recorded as $570 in both Cash and Sales accounts.

Correction: Dr Cash $180 | Cr Sales $180 (the difference: $750 − $570)

5. Complete Reversal of Entries

Both the debit and credit entries are made to the correct accounts but on the wrong sides.

Example: Cash paid for rent of $400 was recorded as Dr Rent $400 | Cr Cash $400, but the entry was actually: Dr Cash $400 | Cr Rent $400.

Correction: Dr Rent $800 | Cr Cash $800 (double the original amount to reverse and re-record)

6. Compensating Error

Two independent errors cancel each other out, so the trial balance still agrees. Both errors must be corrected separately.

Example: Purchases is overstated by $200, and Sales is also overstated by $200. These two errors cancel each other.

The Suspense Account

When the trial balance does not agree, a Suspense Account is opened to temporarily hold the difference. The Suspense Account is a placeholder — it should always be closed to zero once all errors are found and corrected.

Example:

Trial balance shows debit total exceeds credit total by $400. A Suspense Account is opened with a credit balance of $400.

Investigation reveals: Commission received of $400 was entered on the debit side of the Commission Received account instead of the credit side.

Correcting entry: Dr Commission Received $800 | Cr Suspense $800

(The $800 reverses the wrong debit entry of $400 and records the correct credit entry of $400 — together $800 on the debit side of Commission Received.)

Effect of Errors on Profit

Some errors affect the calculated profit figure even though the trial balance may agree. To find the corrected profit:

- Start with the reported profit.

- Add back any expense that was overstated.

- Deduct any income that was overstated.

- Add any income that was understated.

- Deduct any expense that was understated.

Common Suspense Account Mistakes

- Identifying the wrong type of error — read the question carefully and check whether the trial balance was affected.

- Forgetting to double the amount for complete reversal of entries — you must reverse the wrong entry AND record the correct entry, so the correction is twice the original amount.

- Not closing the Suspense Account to zero — after all corrections, check that the Suspense Account balances to zero.

- Confusing errors that affect profit with those that do not — only errors involving income or expense accounts affect profit.

Practice Questions

- A credit purchase of $600 from supplier Wong was completely omitted from the books. Write the correcting journal entry.

- Cash received from customer Ng of $250 was credited to customer Chan's account. Write the correcting journal entry.

- The trial balance shows a difference of $300 (debits exceed credits). A Suspense Account is opened. A sales return of $150 was credited to the Sales account instead of the Sales Returns account. Write the correcting entry and show the Suspense Account.

- Office furniture costing $1,800 was debited to Repairs and Maintenance. What type of error is this? Write the correcting entry.

- Explain why a compensating error does not affect the trial balance but still requires correction.

Students who need help with correction of errors and suspense accounts can find focused support through Strong-Willed Tutoring Services's O-Level POA tuition programme. View our tuition fees to get started.

Conclusion

Correction of Errors is a problem-solving topic that requires logical thinking and strong double-entry bookkeeping skills. At Strong-Willed Tutoring Services, students practise identifying all six error types and writing correcting journal entries using real O-Level examination questions, building both speed and accuracy.